• 13 May 2026

Table of content

Which Loan App Is Best For Self-Employed Without Income Proof?

How To Check Approval Rates For Non-Salaried Loan Applicants?

What Are The Best Income Proof Alternatives For Freelancers?

Which Platforms Serve Self-Employed Borrowers With Low CIBIL Scores?

How To Compare The Real Cost Of Loans For Small Business Owners?

Wrapping Up: Making the Final Choice for Your Business Growth

For years, the Indian credit system had a "salary-slip" obsession. If you were a freelancer, a digital creator, or a small shop owner, getting a loan from a traditional bank felt like trying to solve a puzzle with missing pieces.

Banks wanted a monthly payslip and a Form 16 that most independent workers simply don't have. This "salary-slip" barrier left millions of talented self-employed professionals, including the high-earning individuals in the cold.

However, with the rise of the gig economy, a new wave of fintech platforms has emerged to bridge this gap. Some instant personal loan apps, like mPokket, specifically offer loans for self-employed professionals and those without a traditional corporate background.

Here is how you can navigate this landscape and find the best instant loan apps for self-employed individuals.

Follow our Whatsapp Community for more offers and updates.

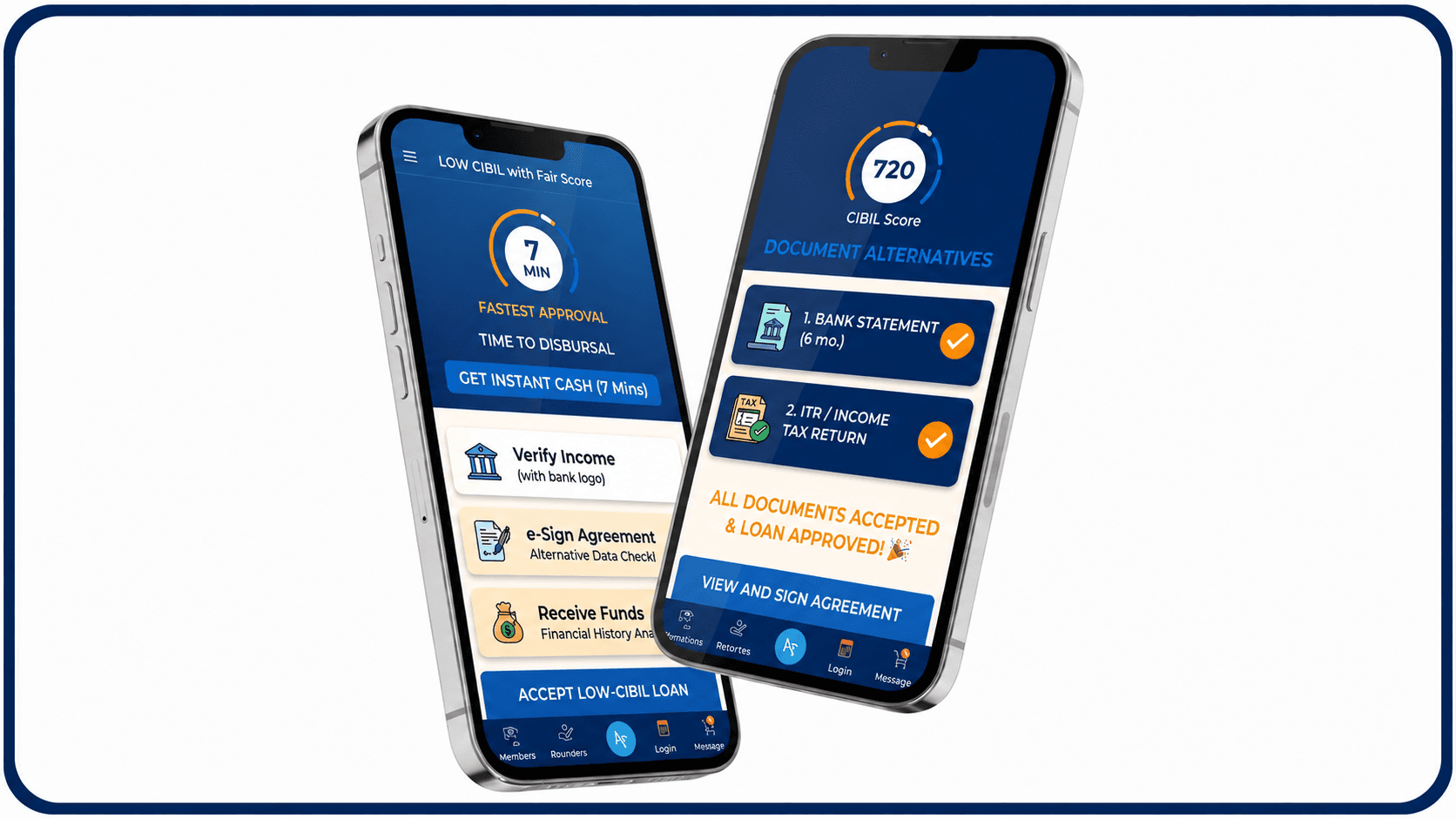

Join nowThe best loan app for self-employed individuals is one that prioritizes digital cash flow over physical salary slips. With that said, mPokket has become a top choice due to its flexible documentation requirements and instant disbursals. In short, those apps you can consider that offer high approval rates based on bank statements and UPI transaction history rather than just corporate employment.

Why salary slips are no longer the only way to prove income?

We’ve moved into an era of "digital footprints." Financial institutions used to rely on physical paper because it was easy to verify. Today, your digital transactions tell a much more accurate story of your financial health. By looking at how money moves through your accounts, many digital lenders can verify your income without ever asking for a piece of company letterhead.

Using bank statements as a primary verification tool

Many apps analyze your bank statements to understand your earning patterns. Whether you get paid by five different clients or one big retainer, these platforms look at your average monthly balance and consistent inflows. This "cash flow-based lending" is a lifesaver for anyone looking for an instant loan without salary slip.

To find an app with high approval rates, look for platforms that mention "alternative credit scoring" and offer small initial ticket sizes to new borrowers. High approval rates are typically found in apps that don't just rely on a CIBIL score but evaluate your real-time ability to repay through digital behavior.

The role of "Alternative Credit Scoring"

Modern AI algorithms are incredibly smart. They don't just look at your credit history; they look at "alternative data" like your utility bill payment consistency and even your UPI transaction frequency. This provides a 360-degree view of your financial discipline, allowing apps to approve loans for freelancers who might have been rejected by traditional banks.

Why smaller ticket sizes lead to higher approval chances?

If you are a first-time borrower, the smartest strategy is to start small. Applying for a massive loan immediately can be a red flag. By taking a smaller amount, like ₹2,000 to ₹10,000, and paying it back on time, you can build a "trust score" within the app. This unlocks higher limits and better interest rates over time.

If you are seeking freelancer loan, the best alternatives to salary slips are ITR (Income Tax Return) filings, GST certificates, and 6-month digital bank statements. These documents prove your business's legitimacy and financial stability, helping you secure larger loan amounts.

Leveraging ITR and GST filings for higher limits

If you want to move from small "emergency" funds to larger business capital (up to ₹2,00,000), showing your ITR is the way to go. It proves that you are a tax-paying professional with a stable income. Similarly, a GST filing acts as a formal "ID card" for your freelance business, making you a very attractive borrower for top-tier apps.

Using client contracts and invoices as credibility proof

Always keep a clean digital folder of your client contracts and paid invoices. While not all apps "read" these automatically yet, having them ready for manual verification can significantly boost your credibility. It shows that your income isn't just a one-time fluke, but a recurring business model.

The best platforms for those with low or "thin" credit scores are specialized fintech apps like mPokket, which are built to be "new-to-credit" friendly. Unlike banks that demand a 750+ score, these apps focus on your current repayment capacity and digital honesty.

Identifying "New-to-Credit" friendly apps

Most young freelancers or gig workers have a "thin" credit file simply because they've never taken a loan before. Traditional banks see this as a risk, but modern apps see it as an opportunity. Look for apps that explicitly state they welcome first-time borrowers or students, as their underwriting models are designed to be more inclusive.

How mPokket supports the gig economy

mPokket has carved out a specific niche for the gig economy. By creating categories for self-employed individuals and small shop owners, they’ve tailored the user experience to those who don’t fit the 9-to-5 mold. Their system is optimized for speed, often getting you from "App Download" to "Cash in Bank" in less than 10 minutes.

Read to know more about - How First-Time Borrowers Can Build Credit History in India?

The most effective way to compare loan costs is to look at the Annual Percentage Rate (APR) rather than just the monthly interest rate. You should also verify if the app allows for early repayment without charging you "foreclosure" or "pre-payment" fees.

Calculating the APR (Annual Percentage Rate)

Interest rates can be deceptive. An app might say "only 2% per month," but once you add processing fees and GST, the real cost is much higher. The APR represents the total cost of the loan over a year. Always compare the APR across apps to see who is actually offering the cheapest deal for your income proof for self-employed status.

Checking for hidden pre-payment penalties

Freelance income is often "lumpy". So, you might have a dry month followed by a huge payout. When that big payout hits, you might want to close your loan early. Some apps will charge you a penalty as ‘Foreclosure Charge’ for doing this. Look for platforms that offer the flexibility to pay off your debt as soon as you have the funds, without extra charges.

Borrowing For The First Time? Explore 7 Financial Terms You Should Know!

Choosing the right financial partner is about more than just a quick cash injection; it’s about finding a platform that grows with you. When comparing, prioritize platforms that offer document flexibility, transparent APRs, and a clear path to higher credit limits.

mPokket stands out by closing the gap for self-employed users who are often ignored by the big banks. With its ability to process loans in under 10 minutes and a deep understanding of the Indian gig economy, it’s a powerful tool for any freelancer looking to manage their cash flow.

Whether you’re scaling your business or covering a short-term gap, the right app should feel like a partner, not a hurdle. Apply Now!

How To Get ₹50,000 Loan On Aadhaar Card?

30 April 2026