4 min read • 14 July 2026

Table of content

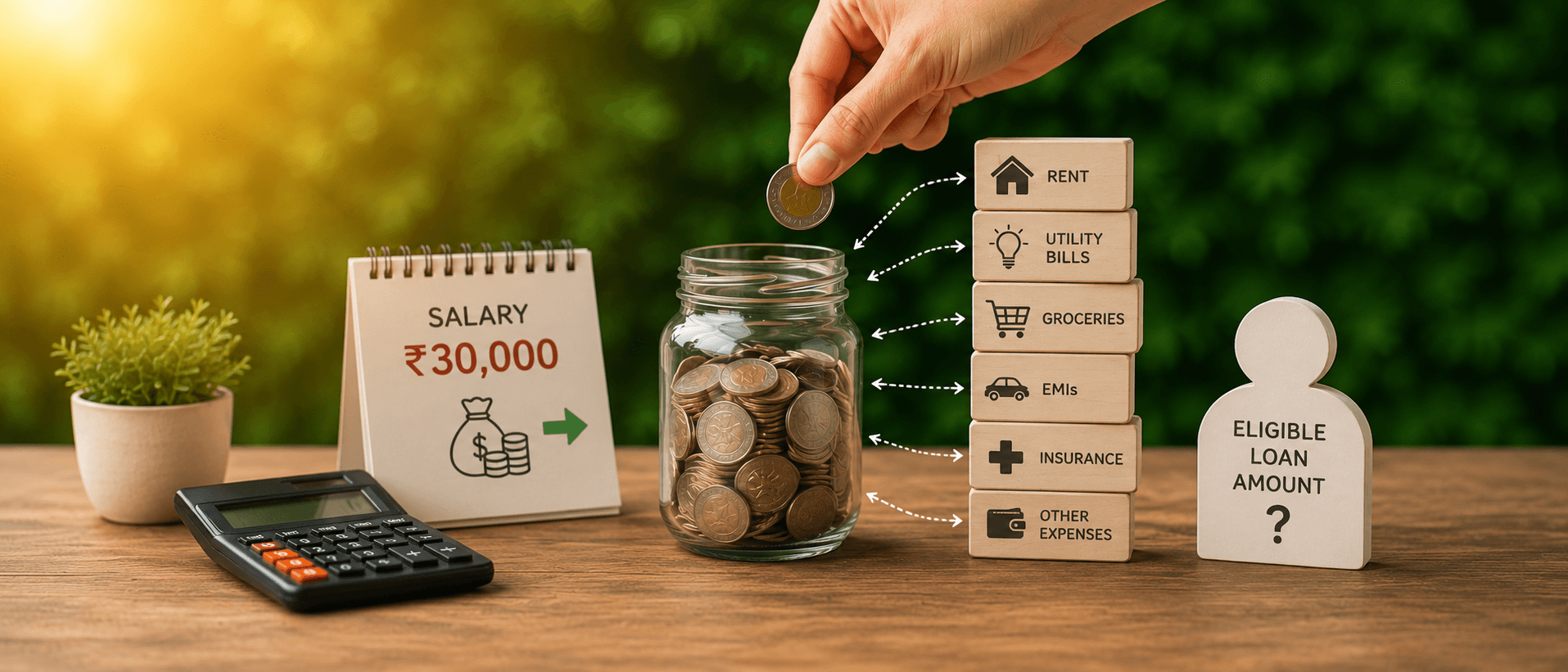

Know What Determines Your Loan Amount Beyond Your Salary.

How Personal Loan for ₹30,000 Salary is Calculated?

How Personal Loan Eligibility is Calculated on a ₹30,000 Salary

What Is FOIR and How Does It Affect Personal Loan Eligibility for 30000 Salary?

What Are the Interest Rates for a Personal Loan Based on Salary of ₹30,000?

How Much Personal Loan Can I Get on 30000 Salary? A Quick Snapshot

How Can Salaried Employees Get an Instant Personal Loan Without a Perfect CIBIL Score?

Conclusion

Frequently Asked Questions

Earning ₹30,000 a month and trying to figure out how much personal loan can I get on a 30000 salary? Honestly, you can get somewhere between ₹1.5 lakh and ₹3 lakh, though it really comes down to your lender, your existing EMIs, and your credit score.

There isn't one fixed number that applies to everyone. Sure, banks and NBFCs look at your salary first. But they're also quietly checking your monthly obligations, how you've handled credit in the past, and whether your job feels "stable" enough on paper. Two people earning the exact same ₹30,000 could walk away with very different offers.

Suppose you earn ₹30,000 a month, have no existing loans, and hold a CIBIL score of 760. Banks, NBFCs, or digital lenders can sanction you ₹2.4 lakh without much back-and-forth. Now compare that to your colleague with the same salary but already paying ₹8,000 toward a car EMI. He will be eligible for a loan amount dropped to around ₹1.2 lakh.

So in this guide, we'll walk through exactly how lenders calculate personal loan eligibility for a 30000 salary, what pulls your number up or down, and where you can turn if your salary slip isn't picture-perfect or you're still building your credit score.

Follow our Whatsapp Community for more offers and updates.

Join nowMost lenders decide personal loan eligibility for 30000 salary based on their internal policy. Standardly, they lean on a simple multiplier, somewhere between 10 and 24 times your monthly income. That's a wide range, and honestly, a few things end up deciding where you land:

Here's the formula lenders usually run with: eligible loan = monthly salary × multiplier (typically 10-24). Now, do that math on ₹30,000, and you’ll be eligible to get loan approval for anywhere from ₹3 lakh to ₹7.2 lakh on paper. However, your actual EMI capacity usually brings that number back down to earth.

The multiplier's only half the story. Personal loan eligibility for 30000 salary also hinges on how much of your income is already tied up in other EMIs and monthly expenses. This is what really decides your final credit limit with the selected digital lender. Here's what typically goes into the eligibility check:

Lenders almost always calculate eligibility on your net take-home pay, not your gross CTC. If your ₹30,000 already has deductions for PF or tax, that's the number that matters.

A salaried employee at a stable company usually gets a smoother approval than a contractual worker earning the same ₹30,000, purely because job continuity reassures the lender.

FOIR stands for Fixed Obligation to Income Ratio, which is just a percentage of your monthly income that's already dedicated for existing debts and fixed expenses, like rent, utility bills, etc. Most lenders want this fixed expense to stay under 40-50%, even once your new EMI joins the mix.

Here's a rough example to make it click. If your salary is ₹30,000 and you're already paying ₹6,000 toward an existing EMI, that's a 20% FOIR. A lender might allow your total obligations to touch 50%, meaning you have room for roughly ₹9,000 more in EMI, which translates to a decent loan amount depending on tenure.

And honestly, this is the real crux of how much personal loan can I get on 30000 salary. It's not really about the salary number by itself. It's about what's left over once your current commitments are accounted for.

Here is how FOIR affects loan eligibility:

Interest rates for a personal loan based on salary of ₹30,000 per month typically fall between 10% and 24% per annum, and where exactly you land depends a lot on your credit score and who you're borrowing from.

Banks generally offer better rates than NBFCs or app-based lenders, but they have strict eligibility rules about documentation and a long, healthy credit history.

Worth checking your score before you start applying anywhere, since even a small bump can shave off a meaningful chunk of interest.

NOTE: A strong credit score can reduce your interest rate, so it's worth checking your score before you start applying anywhere.

Most lenders will sanction somewhere up to ₹3 lakh instant personal loan for salaried person, whose monthly income is around ₹30,000. If your credit score's strong with no existing EMIs weighing you down, that number can stretch up to ₹7 lakh.

Here's a quick snapshot before we get into the details:

Numbers like these shift from lender to lender, so treat this as a ballpark rather than a guarantee. Let's break down exactly how each of these figures gets calculated.

Read to know more about - How to Get a Personal Loan With a Low CIBIL Score

Not everyone earning ₹30,000 walks around with a spotless credit file, and that's exactly where mPokket has been helping people. We offer instant personal loan for salaried employees by looking at alternative data instead of relying solely on your CIBIL score.

Freshers, interns, small business owners, and even salaried persons with entry-level salaries often get turned away by traditional banks, not because they can't repay but simply because they haven't built up a long credit history or don't have formal income proof to show. mPokket doesn't work that way. Here is why you can choose mPokket:

If your salary slip looks thin or your credit score isn't where you'd like, that doesn't automatically shut the door on borrowing.

Read to know more about - How Can You Get an Instant Cash Loan with a Low Salary?

A modest salary or a thin credit file shouldn't be what stands between you and the funds you actually need. If you're still wondering how much personal loan can I get on a 30000 salary, here's the real answer. It depends less on your payslip number and more on where you choose to apply.

Apply for an instant personal loan for salaried employees with mPokket today and get up to ₹2 lakh, even without a perfect CIBIL score.

Interest rates for a personal loan for salaried employees usually start around 10.5% with banks and can climb to 24-30% with NBFCs or instant loan apps. However, it really depends on your credit score and the lender's own policy.

You'll generally need to be a salaried employee aged 21-58, with a reasonably low FOIR, a stable job, and ideally a credit score above 700, though some lenders relax this last condition.

You can, but the amount you're eligible for will shrink based on what you already owe. Lenders work this out through your FOIR, so the less debt you're carrying, the higher your personal loan amount tends to be.

If the co-applicant has a steady income, the lenders will consider your combined earning power and increase your credit limit.

Personal Loans for Salaried Employees: What you Need to Know

5 min read • 9 July 2025

What is the Minimum Salary Needed to Qualify for a Personal Loan?

3 min read • 13 July 2026

Tips for Getting a Personal Loan with a Low Salary

5 min read • 6 December 2024

What are the Key Factors Lenders Consider When Making Low-Salary Instant Loans?

2 min read • 9 July 2025