4 min read • 11 May 2026

Table of content

What Is Mobile-First Lending in India?

Why Are Mobile Loan Apps Growing So Fast in India?

How Do Mobile Loan Apps Work In India?

How is Mobile Lending Bringing More Equality in Rural India?

How Is Mobile Lending Benefitting Young Professionals And Students?

How Are Small Ticket Loans Improving Financial Inclusion In India?

What are The Best Practices of Responsible Digital Borrowing?

How Is RBI Regulation Protecting Mobile Loan App Users?

Why Are Regulated Apps Safe For Borrower Data?

Future Of Mobile First Lending Platforms In India

Conclusion

The credit journey for the Indians has moved from visiting physical bank branches with dozens of documents to super-fast websites, and finally, straight to our phones. In 2026, millions of Indians apply for loans right from their smartphones.

In this blog, we’ll explore the latest trends in digital lending India, how instant loan apps are bridging the rural-urban divide, and how RBI-regulations and digital financial literacy are shaping a secure financial future.

Follow our Whatsapp Community for more offers and updates.

Join nowMobile-first lending refers to the loan journey that begins from the loan application stage until repayment, being entirely on one’s smartphone. Simply put, this is an entirely paperless process created for people who love doing everything through their smartphones.

With the integration of digital platforms, Aadhaar, UPI, and DigiLocker, users can go through the entire loan process from the comfort of their smartphones.

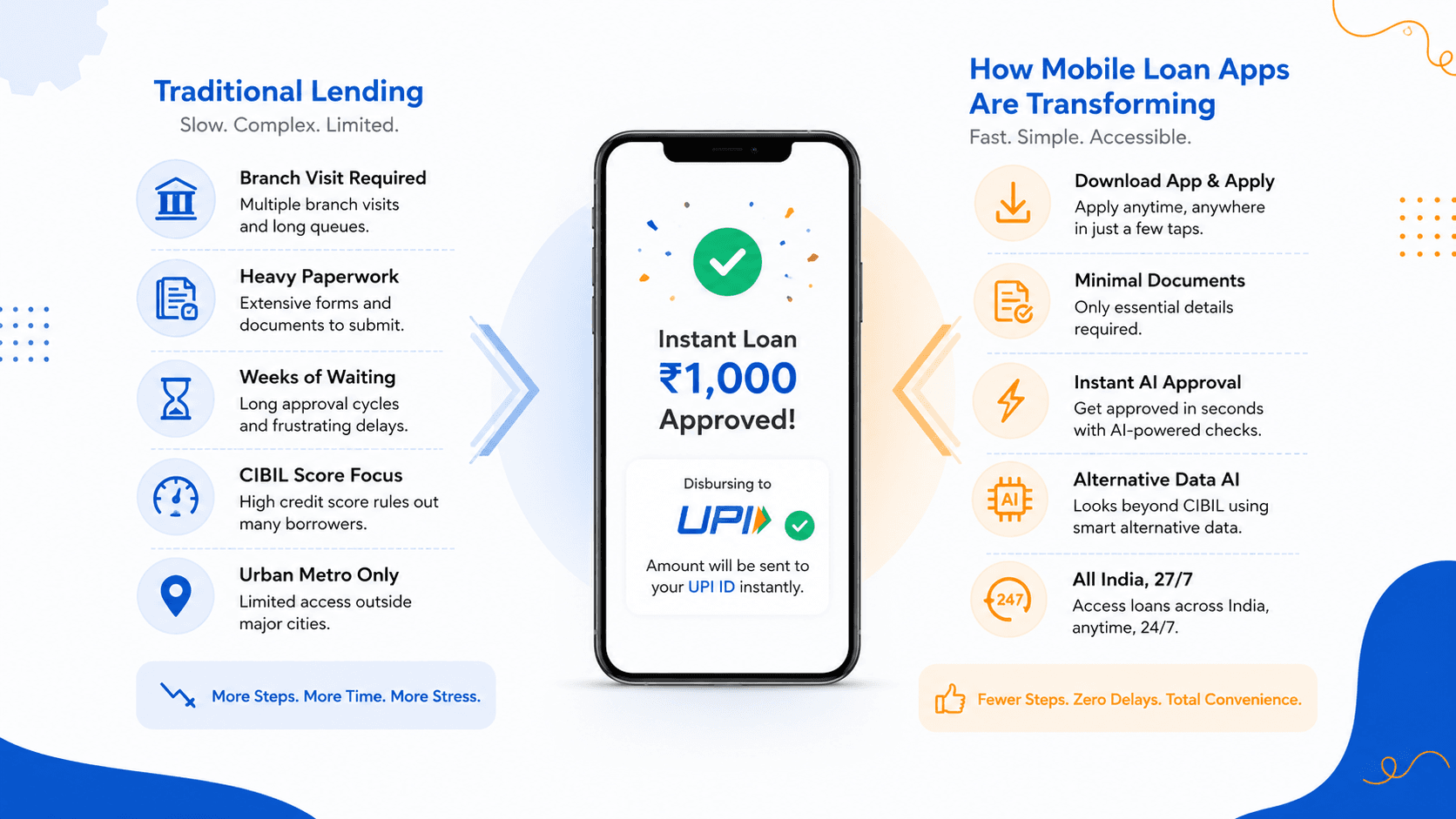

Unlike traditional lending, where users had to visit branches and deal with heaps of documentation, even the initial wave of digital lending required the involvement of computers and manual uploading of paperwork.

There is no denying the popularity of mobile loan apps in India. This is due to several reasons:

UPI has already accustomed Indians to digital transactions. Indians even pay for chai, grocery bills, autorickshaws, and other small expenses using their phones in order not to rummage through their wallets in search of loose change.

Instant loan apps employ automated algorithms to analyse your ability to repay the loan based on the data stored on your phone. Automated credit scoring allows lenders to approve borrowers almost instantly and quickly disburse money to the lender's bank account within a few hours. Let's understand how the process of modern borrowing takes place.

What is the mobile loan journey from download to disbursal?

The application process for taking a loan from the mobile finance app is as follows:

What documents and alternative data are checked in mobile loans?

In order to be eligible for instant loan disbursal, borrowers are required to submit only basic information, namely PAN and Aadhaar card. The apps also review other types of data, including the financial behavior of the user, i.e. bank transactions, utility bill payments, expenses, etc.

If users can submit their salary slip or CIBIL score of 750+ with a positive history of loan repayment, they stand a chance to receive higher limits. However, the instant loan apps provide loan disbursal to even those users who do not have regular income. This is done by analysing their digital footprint and consistent payments from financial apps.

How do instant approvals occur within minutes?

Instant approvals are a result of an efficient credit scoring algorithm. With UPI-enabled credit, lenders can immediately access information regarding the income of users. Additionally, the usage of alternative data makes the loan process convenient for the new borrowers, who lack any traditional credit history.

For many years, rural residents were excluded from formal credit services because of the inability to visit physical bank branches and lack of credit history. Lack of proper documentation, like collateral or salary slip, also hindered access to formal financial services.

Mobile lending helps overcome these challenges due to eKYC enabled through the Aadhaar and the paperless process of loan approval. Nowadays, a villager can take a loan using his or her smartphone. Additionally, the loan amount offered by the apps is small, thus avoiding the risk of imposing huge interest rates on poor villagers as done by informal instant money lenders.

Read to know more about - Financial Inclusion In India.

The needs of young earners are mostly urgent and relatively low. Be it paying for the security deposit on a new apartment or attending a professional course, young professionals usually need money instantly. The loan apps provide unsecured loans for freshers and interns starting from ₹1,000 and reaching up to a few lakhs.

However, banks would hardly lend money to salaried individuals without a CIBIL rating. Hence, there is a big gap left in the market which the mobile lending helps fill by assessing the earning capacity of borrowers. The apps also lend money to freelancers and self-employed persons by analysing their earnings from various sources.

Sachet loans are the smallest ticket loans ranging between ₹500 to ₹50,000 in India. These loans are highly popular among Indian customers due to easy repayment process and non-binding period of contract. The mobile lending apps provide sachet loans that serve as a driving force behind financial inclusion.

Why are Sachet Loans Popular Among Young Borrowers?

Young borrowers often prefer these loans because of the perfect fit of the concept with the "buy now, pay later" mentality. Users can manage minor monthly expenses with ease.

Are sachet loans driving micro-entrepreneurship in small towns?

In Tier 2 and Tier 3 cities, sachet loans facilitate micro-entrepreneurship because such small amounts are needed by the owners of small businesses to buy inventory.

How sachet loans assist users in creating credit history?

Small loans borrowed and paid on time gradually build up a positive credit history. It will come in handy when seeking for home and auto loans in the future.

Read to know more about - How A Small Money Loans Can Help You Build Credit History?

First and foremost, it is important to educate yourself about digital borrowing. Here is a simple checklist to ensure safe borrowing in 2026.

Nowadays, financial security and reliability have taken centre stage due to the rise of online lending platforms. The Reserve Bank of India has introduced stringent digital lending guidelines in order to prevent any kind of fraud and unethical practice from affecting borrowers.

All the lenders in India have been asked by the RBI to fully disclose their partner NBFCs or banks, interest rates charged and other charges involved. The transactions have to take place directly between the app and the customer's bank accounts. A borrower also gets a cooling-off period during which he/she can opt-out of the loan.

All regulated apps have to strictly adhere to data privacy policies. They will not access any unnecessary data from your phone, including your contact list or the gallery. Regulated apps also ensure banking-level encryption so that your personal and financial details are always safe.

For identifying regulated loan apps, one can look for disclosures of the partnering NBFCs on their website as well as in Google Play Store.

The future of mobile lending will be dominated by artificial intelligence-driven credit scoring. Traditional methods of scoring will give way to data insights that enable the lender to understand income trends, expenditure and loan repayment capacity of customers.

Hyper-personalisation is another trend that we are seeing now. In the coming years, loan apps will provide suggestions about credit limits, repayment terms and even the interest rate according to the borrower's financial behaviour. Loan applications will start tailoring themselves to your needs.

Embedded finance and expanding in Tier 2 and Tier 3 cities is yet another trend. Soon, there will be credit options embedded within other apps used by the borrower such as travel, retail or educational. With smartphone usage increasing beyond metropolis cities, mobile-first lending will continue reaching millions of customers in the coming years.

The growing digital financial literacy among borrowers has increased their confidence level. Modern lending practices have improved transparency which is helping in creating better credit culture.

Mobile-first lending platform like mPokket is a shining example in the current credit industry because it combines all the advantages of instant apps. Not only are the processes of approval speedy, but the minimum documentation required has made borrowing more convenient. The easy availability of small ticket size loans and great user experience make mPokket one of the best loan apps in India right now.

If you have always shied away from digital credit, then mPokket is the right choice for you.

Which Is The Most Trusted Loan App In India?

4 min read • 1 May 2026

Need ₹10,000 Urgent Loan Today — What Should You Do To Get It Fast?

4 min read • 30 April 2026

How To Get ₹50,000 Loan On Aadhaar Card?

4 min read • 30 April 2026

7 Financial Terms Every First-Time Borrower Should Know in India

4 min read • 7 May 2026

What Young Professionals Should Know About Borrowing Before Taking a Loan

4 min read • 7 May 2026